Why Rental Income Tax Kenya Matters for Every Property Owner

Let's be honest—discussing taxes is rarely anyone's favourite pastime. However, getting to grips with rental income tax in Kenya is more than just ticking a compliance box. It's a crucial step in protecting your property investment and securing its future profitability. Whether you're renting out a single bedsitter in Roysambu or managing commercial units in Westlands, this tax directly shapes your financial returns. Ignoring it is like building a house without a solid foundation; it might stand for a while, but problems are inevitable.

Think of your rental property as a business. A shopkeeper tracks every sale and expense, and in the same way, a landlord must account for rental income and the taxes that come with it. When you understand this system, it stops being a source of stress and becomes a predictable part of your business strategy. This knowledge helps you set the right rent, budget for expenses, and plan your next property investment with confidence.

From Legal Requirement to Financial Reality

The idea of taxing rental earnings isn't new. In fact, rental income has been a taxable source of income since the Income Tax Act of 1973. Despite this long-standing law, many landlords didn't comply for years. Studies from 2012 showed that less than 40% of landlords and property developers were following the rules. You can dive deeper into this history in the official KESRA journal.

That gap between the law and what people actually do is closing fast. The Kenya Revenue Authority (KRA) has stepped up its efforts, using data from multiple sources to find property owners who aren't paying their fair share. For the modern landlord, the question is no longer if you need to pay, but how to manage it smartly. From the matatu driver renting out a family home to the investor with a large property portfolio, everyone is now expected to be compliant.

Protecting Your Investment and Bottom Line

Managing your rental tax obligations is a core strategy for protecting your assets. Landlords who don't comply risk heavy penalties, interest on unpaid taxes, and even legal trouble. All of these can wipe out years of rental profits. Imagine getting a bill for several years of back taxes plus penalties—it could be financially devastating.

On the other hand, a compliant landlord enjoys peace of mind. You can deal with tenants confidently, get loans for new projects, and build a strong reputation in the property market. By understanding the regulations, you can also legally reduce your tax bill by claiming all allowable expenses, a topic we will cover later. For landlords looking to streamline their operations, exploring property listings and management resources available online can provide useful tools. Ultimately, viewing rental tax as a key part of your business strategy is the first step toward lasting success in Kenya's property market.

Breaking Down Kenya's Rental Income Tax Rates Made Simple

Forget trying to decipher dense legal documents and confusing tax schedules; let's discuss what you, as a landlord, actually need to pay. Understanding the rates for rental income tax in Kenya is like learning the rules of a game you're already playing. Getting it right means you can budget properly and avoid any unwelcome surprises from the taxman.

The amount of tax you owe isn't a one-size-fits-all figure. It hinges on a few key factors, primarily your total rental income and whether you're a resident individual, a non-resident, or a registered company. Think of it as different pricing tiers for a service—your tax rate is tailored to your specific situation. The Kenya Revenue Authority (KRA) treats a local landlord differently from a foreign investor or a large property management company, a distinction that directly shapes your final tax bill.

Individual vs. Corporate Tax Rates

The most important distinction the KRA makes is between individual landlords and corporate entities. Each group is subject to a different tax structure, which determines how their rental income is taxed.

- For Individuals: If you're a resident individual earning rental income, the tax is typically calculated using progressive bands. This means the percentage of tax you pay increases as your income grows.

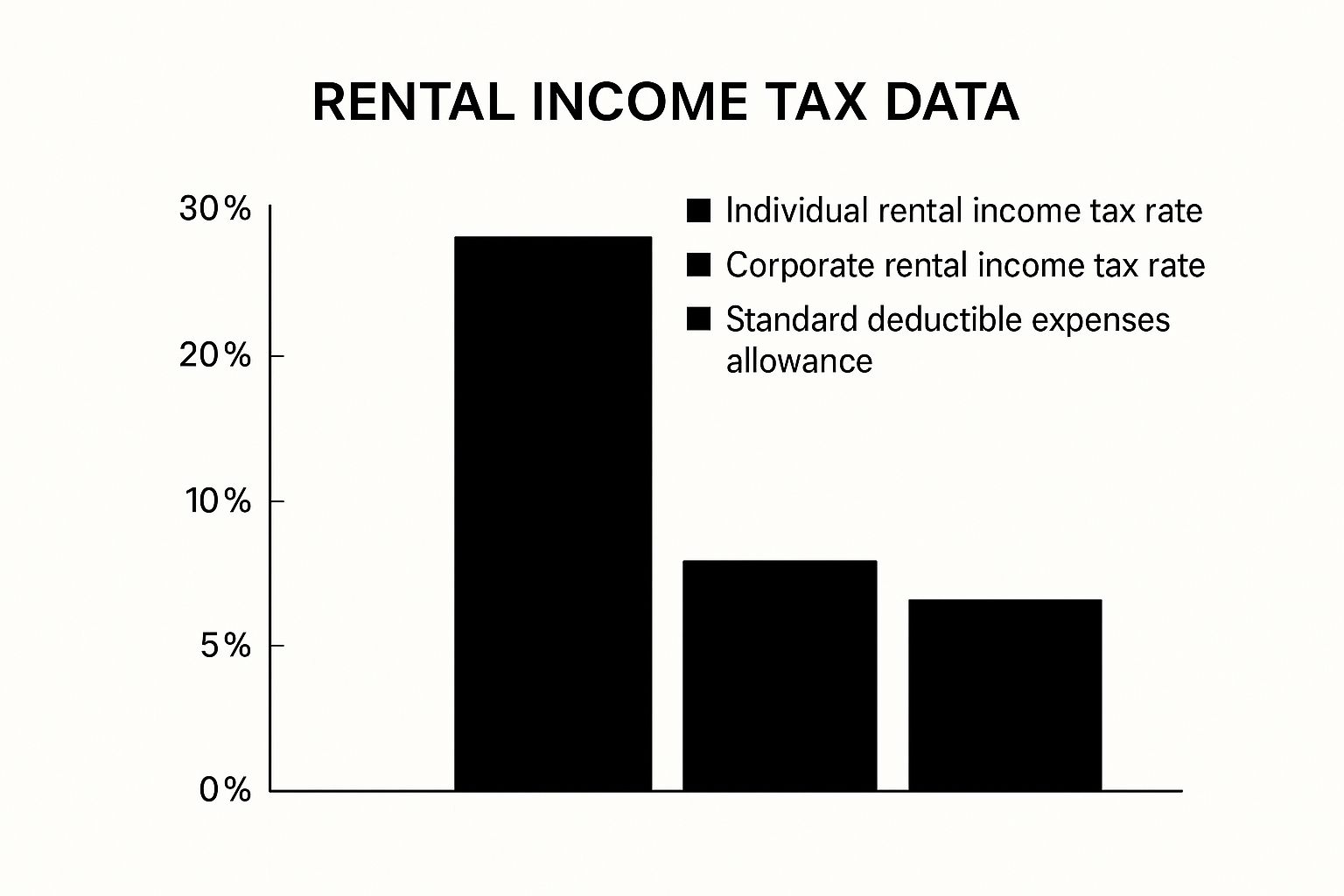

- For Companies: A company that owns and rents out properties faces a more straightforward calculation. Its net rental profits are subject to the standard corporate tax rate, which is currently a flat 30%.

To help you visualise these differences, we've put together a table that breaks down the rates for various taxpayer categories.

| Taxpayer Category | Income Range (KShs) | Tax Rate (%) | Additional Notes |

|---|---|---|---|

| Resident Individual | Monthly Residential Rental Income: 24,001 - 333,333 | 7.5% | This is the Monthly Rental Income (MRI) tax, a simplified final tax on gross rent. Applies if annual income is between KShs 288,000 and KShs 15,000,000. |

| Resident Individual | Annual Income (PAYE Rates) | Progressive (10% - 35%) | This applies if you opt out of the MRI or your annual rental income is below KShs 288,000 or above KShs 15,000,000. |

| Company | All Net Rental Profit | 30% | This is the standard corporate tax rate applied after deducting allowable expenses from gross rental income. |

| Non-Resident | All Gross Rental Income | 30% | This is a final withholding tax. The tenant or agent must deduct and remit it to the KRA. |

This comparison highlights that while companies have a fixed rate, individuals have different options and thresholds to consider, making it important to know which category you fall into.

The following infographic provides a quick visual comparison of the key rates that affect Kenyan landlords.

As the chart illustrates, a company's tax liability is calculated at a flat rate, whereas an individual's tax journey can be more layered, depending on their income level and filing choices.

Understanding the Progressive Scale for Residents

For resident individuals who aren't using the simplified Monthly Rental Income (MRI) tax, the system is not a single flat percentage. Instead, your annual rental income is taxed in slices, with each slice facing its own rate. This is the same Pay As You Earn (PAYE) system used for employment income.

Let's imagine Sarah, a landlord from Nakuru, who earns an annual rental profit of KShs 500,000. Her tax isn't just a simple percentage of that total. It's broken down into brackets. For resident individuals, the first KShs 288,000 is taxed at 10%, the next KShs 100,000 at 25%, and income above KShs 388,000 is taxed at higher rates up to 35%. You can find a detailed breakdown of these brackets in this helpful tax alert from PwC. This tiered system ensures that landlords with lower rental earnings pay a smaller proportion in tax compared to those with higher incomes.

Special Considerations: Non-Residents and VAT

The rules are different for non-resident landlords. If you own property in Kenya but live abroad, your rental income is subject to a withholding tax. This is a final tax, currently set at 30% of the gross rent. Your tenant or appointed agent is legally required to deduct this amount from the rent and remit it directly to the KRA on your behalf.

Furthermore, Value Added Tax (VAT) is another important factor, particularly for commercial properties. If your annual income from commercial rentals exceeds KShs 5 million, you must register for VAT. This means you will need to charge VAT on the rent you collect. While it adds another layer of compliance, it is a standard requirement for managing large-scale commercial property rentals in Kenya.

Calculating Your Rental Income Tax Like a Pro

Turning your rental income into a final tax figure might seem complex, but it's a straightforward process once you understand the steps. Instead of making a guess at what you owe, let's walk through how to accurately calculate your rental income tax in Kenya. We will start with a simple example and gradually build up to more complex situations, giving you the confidence to manage your own tax obligations.

Think of the calculation as a basic formula: Total Rent Received - Allowable Expenses = Taxable Income. This final amount is what the KRA uses to figure out your tax bill based on the rates we have already covered.

Starting with the Basics: A Single Property Scenario

Let's begin with a common example. Imagine you own a single apartment in Nairobi that you rent out for KShs 30,000 per month.

- Gross Annual Income: The first thing you need to do is work out your total rental earnings for the year. This would be KShs 30,000 x 12 months = KShs 360,000.

This annual figure of KShs 360,000 falls neatly into the KShs 288,000 to KShs 15 million bracket for the simplified Monthly Rental Income (MRI) tax. Under this method, the tax is a flat 7.5% of the gross monthly rent. So, your monthly tax would be 7.5% of KShs 30,000, which is KShs 2,250. Annually, this comes to KShs 27,000. The beauty of this method is its simplicity, as it does not require you to track individual expenses.

Handling More Complex Rental Situations

Of course, being a landlord is rarely that simple. What happens if you have variable income or own several properties? Let's say you own two units: one residential and one commercial. This is where tracking your allowable deductions becomes essential, especially if you opt to file an annual tax return instead of using the MRI system.

Consider these frequent scenarios and how to manage them:

- Upfront Payments: If a tenant pays six months' rent in advance, this entire sum is counted as income in the month you receive it. You must declare it then, even though it covers the coming months.

- Vacant Months: Should a property be empty for a couple of months, you simply report zero income for that period. This is a primary reason why keeping careful monthly records is so important. Monitoring vacancies can also help you analyse the performance of your rental properties across different locations.

- Mid-Year Rent Increase: If you raise the rent from KShs 30,000 to KShs 32,000 in July, your calculation needs to reflect this change. You would calculate six months at the old rate and six months at the new rate to arrive at the correct annual gross income.

For landlords with commercial properties or those whose income falls outside the MRI brackets, the calculation involves subtracting allowable expenses from your gross income before applying the progressive tax rates. This demands meticulous record-keeping of costs like agent fees, repairs, and insurance. By getting these calculations right, you ensure you are compliant and maintain full financial control over your investment.

Mastering KRA's iTax System for Rental Income Filing

Filing your rental income tax in Kenya through the KRA's iTax portal can feel intimidating, but it doesn't have to be. With a clear plan, you can turn this task from a source of stress into a standard part of your business operations. This guide will walk you through the digital system, showing you the key steps and helping you sidestep common mistakes that can lead to penalties or delays.

Think of iTax as the official digital desk where you present your rental business records to the KRA. Just like you'd organise your physical receipts before heading to an office, getting your digital documents in order is the first and most important step. The portal is built to manage the entire process, from start to finish, but its effectiveness relies on you providing accurate information.

Your Step-by-Step Guide to Filing on iTax

Your journey begins at the iTax portal, the central hub for all tax-related activities. Before you even start, make sure you have your KRA PIN and password handy. If you've misplaced your password, don't worry; the portal has a simple recovery process to get you back on track.

Here is the iTax login portal, which is your starting point for filing.

This screen is your doorway to managing your tax duties. Having your login details ready is the first small victory in achieving a smooth filing experience.

Once you are logged in, the process typically follows these stages:

- Navigate to the Returns Menu: Look for the "Returns" tab on your main dashboard. Click on it and select the option to file a return from the dropdown menu.

- Select the Correct Tax Obligation: The system will ask you to choose your tax obligation. For rental income, you must select "Income Tax - Rental Income."

- Download the Relevant Form: You will then be prompted to download an Excel-based tax return form. This is the most crucial step. KRA provides different forms for Monthly Rental Income (MRI) and for declaring rental income as part of an annual return. It is essential to download the correct one for your specific situation.

- Complete the Form Offline: Open the downloaded Excel file. When prompted, you must enable macros for the sheet to work correctly. Fill in all the required details, such as your personal information, property specifics, gross monthly rent, and any allowable expenses if they apply to you. Always double-check your figures for accuracy.

- Validate and Generate Upload File: After filling everything out, click the "Validate" button inside the Excel sheet. The form will check for any errors. If your details are correct, it will let you generate a compressed .zip file. This is the file you will upload back to the iTax portal.

- Upload and Submit: Go back to the iTax portal, agree to the terms, and upload the .zip file you just created. Once the upload is successful, you can submit your return. You will immediately receive an acknowledgement receipt, which you should save for your records.

Common Pitfalls and How to Avoid Them

Even with a straightforward process, small errors can create big headaches. Here are some frequent issues landlords encounter:

- Using an Outdated Form: KRA updates its forms from time to time. To avoid issues, always download a new form directly from the portal for each filing period.

- Incorrect Property Details: Make sure all information, like tenant PINs (if required) and property addresses, is entered accurately. Typos can cause validation errors and stop your submission.

- Filing After the Deadline: The deadline for Monthly Rental Income tax is the 20th of the following month. For those filing annually, the deadline is 30th June. Late filing results in penalties, so it's wise to mark these important dates in your calendar.

By following this structured approach and being aware of these common mistakes, you can handle your rental income tax obligations on iTax with confidence and stay compliant with KRA's requirements.

Maximising Deductions and Understanding Exemptions

Every shilling you can legally deduct from your rental income is a shilling that stays in your pocket. Learning how to claim all your allowable expenses is a key strategy for any property owner looking to manage their rental income tax in Kenya effectively. The goal is simple: pay what you owe, but not a single shilling more. While some costs are obvious, many landlords miss out on lesser-known deductions that could significantly lower their taxable income.

Think of your rental property as a business. Any cost you incur purely to generate that rental income can potentially be claimed as an expense. This isn't just about collecting rent; it's about maintaining the property to keep it desirable for tenants and managing it professionally. In this process, smart record-keeping is your best friend, turning potential tax savings into actual cash in the bank.

The Crucial Difference: Revenue vs. Capital Expenses

The Kenya Revenue Authority (KRA) draws a very clear line between two types of spending: revenue expenditure and capital expenditure. Understanding this distinction is fundamental to getting your taxes right.

- Revenue Expenditure: These are the everyday costs of keeping your property running and earning income. Think of them as the 'fuel' for your rental business. They are fully deductible from your rental income in the same year you spend the money. Common examples include routine repairs (like fixing a leaking tap), paying land rates, agent fees, and insurance premiums.

- Capital Expenditure: These are costs for major improvements or additions that significantly increase the property's value or extend its useful life. Imagine building a new extension, installing an entirely new plumbing system, or putting on a new roof. These are not deducted directly from your income all at once. Instead, you claim them over several years through a system called Wear and Tear Allowance.

This distinction is critical. Confusing the two can lead to the KRA disallowing your claims, which could result in penalties and a higher tax bill.

Common Deductible Expenses You Shouldn't Overlook

To help you identify all your potential savings, we've outlined the common allowable expenses you can deduct from your gross rental income when filing your annual return. Before we dive into the list, it's important to remember that you must have proof for every expense. Invoices, receipts, and bank statements are not just good to have—they are essential if the KRA ever decides to audit your returns.

To give you a clear picture of what you can claim, we've created a detailed table. It breaks down the expense categories, lists specific deductible items, and explains the documentation you'll need.

| Expense Category | Deductible Items | Documentation Required | Common Mistakes |

|---|---|---|---|

| Property Management | - Agent's commission for letting and management - Fees for rent collection - Security service costs (if paid by landlord) - Caretaker/cleaner salaries | - Agent's fee notes/invoices - Signed contracts - Payroll records - Bank statements showing payment | - Claiming fees for selling the property (this is a capital expense). - Not having formal agreements with agents or caretakers. |

| Repairs & Maintenance | - Routine plumbing and electrical repairs - Repainting (interior and exterior) - Repairing broken windows or doors - Fixing leaks | - Invoices from contractors (fundis) - Receipts for materials purchased - M-Pesa/bank transfer confirmations | - Classifying major renovations (e.g., a new kitchen) as a repair. - Lacking detailed invoices that specify the work done. |

| Financing Costs | - Interest paid on a mortgage or loan used to acquire or improve the rental property. | - Loan statements from the bank clearly showing the interest portion. - Original loan agreement. | - Claiming the entire loan repayment amount (principal is not deductible). - Claiming interest on personal loans not used for the property. |

| Land Rates & Rent | - Annual land rates paid to the county government. - Land rent paid to the national government (for leasehold properties). | - Official payment receipts from the county/national government. - Demand notes. | - Forgetting to claim these annual payments. - Estimating the amount without official receipts. |

| Utilities | - Water bills paid by the landlord. - Electricity for common areas (e.g., security lighting). | - Utility bills in the landlord's name. - Proof of payment. | - Claiming for utilities that are paid directly by the tenant or recovered from them through service charges. |

| Professional & Legal Fees | - Legal fees for drafting tenancy agreements. - Costs of advertising vacant units. - Accounting fees for preparing rental income accounts. | - Invoices from lawyers or accountants. - Receipts from advertising platforms (e.g., newspapers, online listings). | - Claiming legal fees related to the initial purchase of the property. - Not having clear invoices detailing the service provided. |

| Insurance | - Insurance premiums for policies covering fire, theft, or property damage. | - Insurance policy document. - Premium payment receipts or debit notes. | - Claiming premiums for life insurance or other personal policies. - Failing to renew the policy but still claiming the expense. |

Properly documenting every single one of these expenses with receipts and invoices is non-negotiable. During a KRA audit, these records serve as your evidence. Without them, even legitimate expenses can be rejected, costing you thousands of shillings in avoidable taxes. Keeping a simple spreadsheet or using accounting software can make tracking these expenses much easier throughout the year.

Proven Compliance Strategies That Actually Work

Successfully managing your rental income tax in Kenya isn't about achieving perfection overnight. It's about building simple, consistent systems that prevent stress and keep you on the right side of the Kenya Revenue Authority (KRA). Many landlords who have mastered this process rely on structured routines rather than last-minute scrambling during tax season.

Think of compliance like maintaining a car. You don't wait for it to break down on the motorway; you perform regular oil changes and check-ups. In the same way, a small amount of regular effort in managing your rental finances prevents a major breakdown when filing deadlines approach. This proactive approach turns tax compliance from a feared event into a manageable business task.

Building Your Record-Keeping Toolkit

Your first step is to choose a record-keeping method that fits your needs. This doesn't need to be a complex accounting suite. The best system is the one you will actually use.

- For simple portfolios (1-3 units): A dedicated notebook or a basic spreadsheet can be perfectly fine. Create columns for the date, tenant's name, rent amount received, and any expenses. For expenses, jot down what it was for (e.g., "plumbing repair, unit 2") and keep the physical receipt or a photo of it in a dedicated folder on your phone.

- For larger portfolios: As your property portfolio grows, manual tracking becomes tiresome. Consider using property management apps or software. These tools not only track income and expenses but can also generate reports, manage tenant communication, and send rent reminders. This automates much of the work and creates a clean digital trail.

Regardless of the tool you choose, consistency is crucial. Set aside just 15 minutes every week to update your records. This small habit makes a huge difference.

Handling Real-World Compliance Challenges

Managing a rental property in Kenya comes with unique situations that require smart compliance strategies.

- Cash Payments: A significant number of tenants still pay rent in cash. When you receive cash, deposit it into your bank account promptly. Then, record the transaction in your spreadsheet or app immediately. The bank deposit slip acts as a third-party record of the income, adding a valuable layer of proof.

- Irregular Payments: If a tenant pays late or in instalments, you must record each partial payment on the date you received it. Your records need to reflect what actually happened, not just what the tenancy agreement dictates. This accuracy is vital for both your financial planning and your tax filings.

- Security Deposits: Remember, a security deposit is not income. It is a liability—money you hold on the tenant's behalf. It only becomes income if you have a legal right to keep it to cover property damages or unpaid rent. It's a good practice to keep deposits in a separate account to avoid accidentally treating them as revenue.

To attract dependable tenants and make management easier, many landlords find success when they advertise their properties on reputable platforms, which often attract a pool of pre-screened applicants.

By establishing these simple but effective habits, you create a solid compliance framework. This not only protects you from penalties but also gives you clear insights into the financial health of your property investment, helping you make smarter decisions for the future.

Learning From Others' Costly Rental Income Tax Mistakes

The smartest property owners don't learn from their own expensive mistakes; they learn from the mistakes of others. This is especially true when it comes to managing rental income tax in Kenya. With the KRA watching more closely than ever, a simple oversight can quickly snowball into huge financial penalties, wiping out years of hard-earned rental profits. By understanding the common tripwires, you can build a more robust and compliant property business.

The cautionary tales of landlords who've run into trouble with the taxman often follow similar patterns. These aren't complex tax evasion plots, but rather everyday blunders in record-keeping or understanding that spiral into major issues. Simply ignoring the rules is no longer a sustainable strategy, and seeing where others went wrong gives you a clear map of what to avoid.

Dangerous Misconceptions and Their Consequences

Many of the most expensive errors are born from simple, but dangerous, misunderstandings about how rental tax works. Believing these myths can put you on a direct path to non-compliance and painful penalties from the KRA.

Here are a few of the most common and damaging mistakes:

- Underreporting Cash Payments: One of the easiest traps to fall into is not declaring the full amount of rent received, particularly when tenants pay in cash. A landlord in Nairobi discovered this the hard way when a KRA lifestyle audit flagged a major gap between his declared income and his spending habits. The result was a bill for back taxes and penalties exceeding KShs 500,000.

- Missing Critical Filing Deadlines: Forgetting or putting off filing deadlines is another classic mistake. An investor in Mombasa with a portfolio of beachfront properties missed the Monthly Rental Income (MRI) filing deadline for three months in a row. The combined penalties for late filing and late payment rapidly accumulated, transforming a manageable tax bill into a serious financial headache.

- Claiming Inappropriate Deductions: A property owner in Kisumu attempted to write off the entire cost of building a new perimeter wall as a simple repair expense. The KRA correctly identified this as a capital improvement, disallowed the deduction, and hit him with a new tax assessment plus interest. This story underlines just how important it is to know the difference between routine maintenance and capital expenditure.

The Real Risks of Hiding Rental Income

Trying to operate on a cash-only basis or otherwise hide rental income from the KRA is a high-stakes gamble in today's environment. Increased data sharing between government bodies, utility providers, and banks makes it much easier for the KRA to spot undeclared rental properties. The fallout from getting caught goes beyond just the financial penalties—it can tarnish your reputation and make it harder to get loans for future investments. By learning from these common pitfalls, you can safeguard your assets and your peace of mind.

Finding the right property and managing it well is the foundation of long-term success. To browse a wide selection of rental properties and make your search easier, take a look at the listings on Rentify.

Article Written by DigiTenant